In the third blog of this 9-part series, we will explore the transformative capabilities of Blockchain and Crypto and how it is changing the dynamics of the financial landscape.

People are often confused when they come across the term “Blockchain”. While most digital natives know that it is a breakthrough computer science innovation, there is more to it than just code-based advancements. Blockchain is a powerful tool that enables trust, compliance and decentralisation. So let’s explore what blockchain is in simple terms.

Blockchain Explained

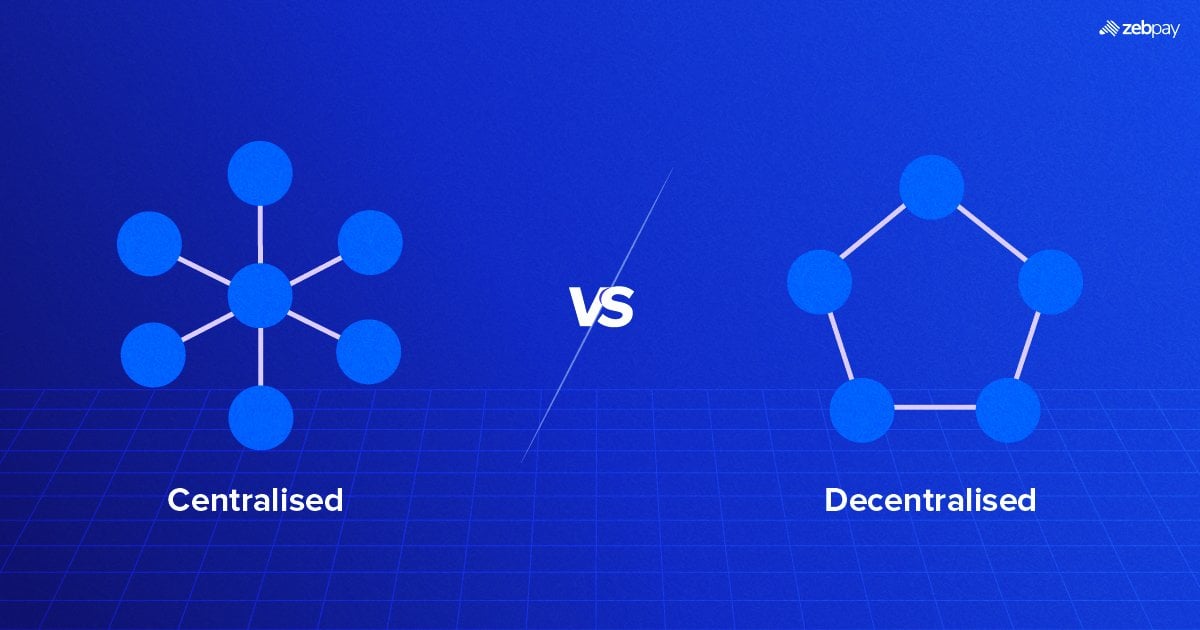

One of the simplest ways to explain blockchain is to think of it as a giant global spreadsheet which is distributed across a network of nodes (computers). All the nodes are equal custodians of the database and they help it function. Instead of having a central authority which acquires, manages and distributes data, blockchain enables collective decision-making to add data to this spreadsheet and validate it.

Blockchain uses state-of-the-art cryptography techniques to keep the data immutable which means that once the data is written on it, it cannot be changed. Cryptography techniques make it permissionless which means that approvals of any centralised entities are not required. The systems of blockchain are designed in such a way that there is no possibility of double-spending.

Read more: What Are Blockchain Layers

Think of it this way, If A transfers INR 100 to B through a centralised banking channel, then the ledgers of the bank accounts of A and B are changed accordingly. However, the catch is that the transactions are monitored by a central authority. In the case of blockchains such as Bitcoin, all the nodes collectively monitor transactions and ensure that there is no double-spending. This is done through a process called Mining. This is a process where miners (nodes) validate transactions using computational power. These systems are designed in such a way that committing fraud on the blockchain is almost impossible as it requires the fraudulent actor to not just manipulate the block on which the transaction is embedded, but also all the blocks prior. This makes committing blockchain fraud nearly impossible and financially unsustainable.

Applications of Blockchain

Blockchains can not only record financial transactions but any kind of structured information. This extended the application of blockchain to not just crypto tokens like Bitcoin but also other virtual digital assets.

Blockchain represents an extraordinary development—an immutable and unhackable distributed database housing digital assets. It serves as a foundation for both truth and trust. The implications are profound, impacting not only the financial services sector but virtually every facet of our society.

Read more: Navratri Crypto Day 02

To learn more about Crypto, Web 3 and Blockchain, visit zebpay blogs. Click on the banner below to join the millions taking part in the Navratri festive celebrations.. Stay tuned for our next blog which will detail “How to Energize your Crypto Portfolio?” in this 9-part series.