The Benefits of Grayscale Crypto Products

One of the most popular methods to get exposure to digital currencies via traditional equities is through Grayscale Trusts. In fact, Grayscale Bitcoin Trust (GBTC) is the largest publicly traded Bitcoin fund in the world with an AUM of $24.6 billion (at the time of this writing).

In addition to GBTC, Grayscale offers other financial products that track other crypto assets (Ethereum, Litecoin, Bitcoin Cash, and others). These are available on the Vested platform and you can find the full list here.

Some institutional and retail investors prefer to invest in these Grayscale products rather than direct ownership of the underlying digital assets for the following reasons:

- Investing in these is more hassle free (no risk and complexities of holding custody of your own digital assets).

- Clearer tax regulations. Because Grayscale shares are traditional securities, there is a clearer tax guidance around their ownership.

- And for some investors, investing in Grayscale products can be more tax efficient. For investors from India, this might be the case. Since April 1st 2022, crypto assets are being taxed at a 30% rate (which cannot be used to offset losses from other crypto transactions). Not only that, after July 1st 2022, an additional 1% TDS (tax deducted at source, which is a form of tax prepayment) will also come into effect.

The Problem of Grayscale Crypto Products

Having said that, there is a ts. common problem plaguing all Grayscale’s products. None of them have achieved their stated investment objectives to track prices of the underlying digital assets.

The problem is two-fold:

- There’s a management fee that ranges from 2 – 2.5%. Grayscale funds regularly sell or distribute digital assets to pay for ongoing expenses. Therefore, the amount of digital assets represented by each share will gradually decline over time.

- Grayscale products have large tracking errors. Grayscale products are structured as Trusts (which for practical purposes are similar to closed-end funds). This means that they cannot efficiently issue new shares or remove shares from the open market to adjust to capital inflow/outflow. As a result, the share price of the Trusts can deviate from the net asset value.

What does this mean? Here’s the percentage return of various cryptos vs. their Grayscale counterparts over the past 1.5 years. The solid dark blue line represents the underlying crypto asset. The light blue line is its Grayscale counterpart. As you can see, tracking is poor, and generally, Grayscale products have been underperforming their crypto counterparts.

Figure 1: Comparison of percentage return of the various crypto assets vs. the Grayscale counterparts. Dark blue lines represent the underlying crypto asset’s performance. The light blue lines represent the Grayscale equivalent. Data is sourced from Yahoo Finance

With persistent tracking errors, you would expect that the deviation should be both in the positive and negative directions. But that is not what we are seeing in Figure 1. Let’s take a deeper look at these tracking errors.

Grayscale products trade at a significant premium or discount for extended periods of time

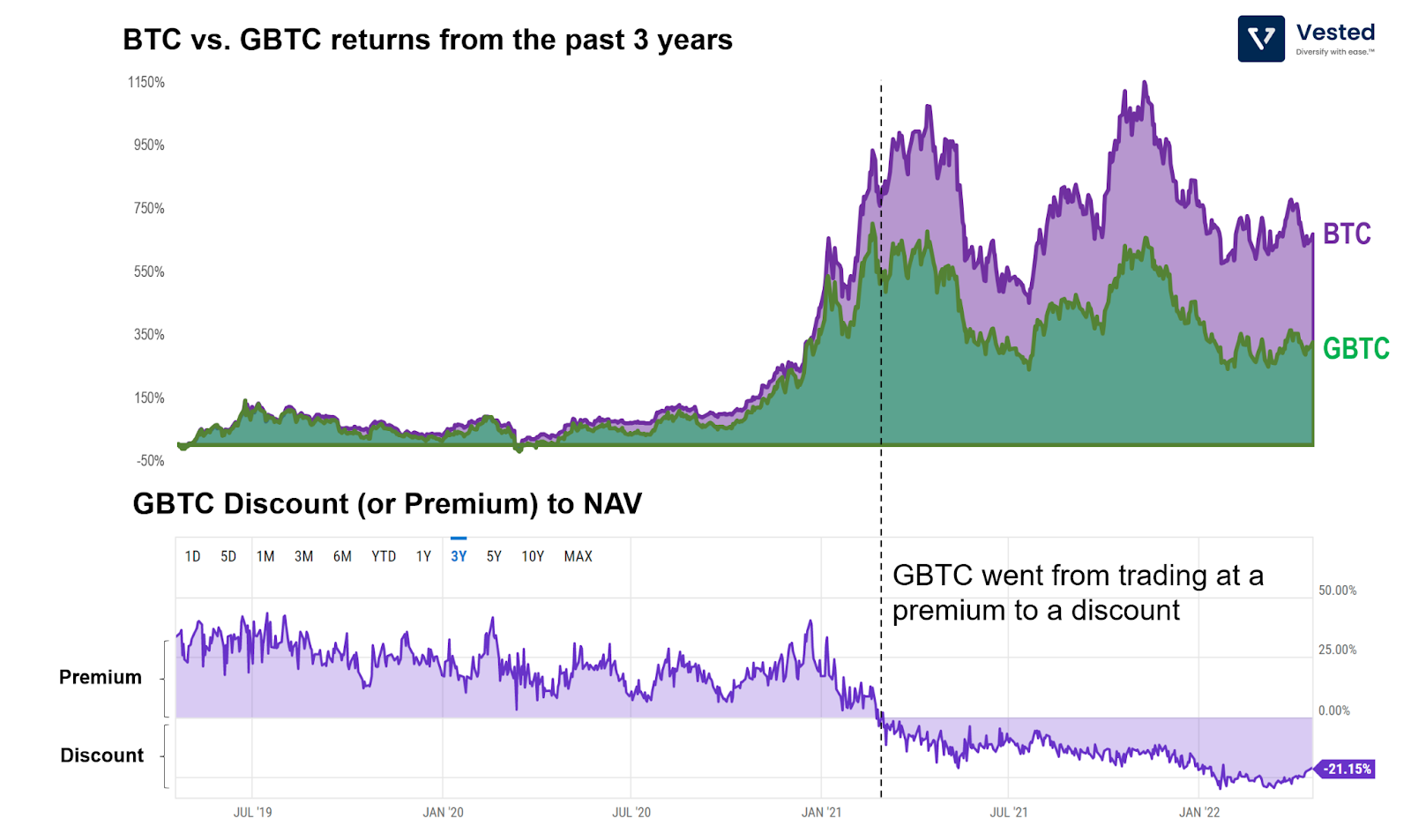

First, let’s take a look at GBTC vs. BTC tracking errors. As mentioned above, the supply/demand imbalance in the GBTC shares leads to tracking errors. Figure 2 below shows the deviation over the past three years for GBTC. It seems that the direction of the deviation tends to be consistent over time.

Figure 2: Three years of GBTCvs. BTC returns and deviation from the native asset value (NAV). Positive deviation means that the GBTC per share value is trading at a premium vs. the equivalent BTC amount. Negative deviation means that the GBTC per share value is trading at a discount vs. the equivalent BTC amount. Source

- When the deviation is positive, GBTC trades at a premium when compared to the spot price of BTC.

- When the deviation is negative, GBTC trades at a discount when compared to the spot price of BTC.

GBTC used to trade at a premium, but that deviation changed to a discount around February 2021. As of this writing, the discount is about 21% compared to the BTC NAV. This means that if you buy $0.79 worth of GBTC shares, you get $1.00 in BTC value.

The transition to a negative premium in February 2021 may be due to two reasons: (1) Grayscale might’ve over issued shares in the past. (2) The launches of two Canadian BTC ETFs around the same time provided additional options for institutional investors to gain BTC exposure.

You can see a similar phenomenon with Grayscale’s ETHE vs. ETH (Etherium). See Figure 3 below.

Figure 3: One year of ETHE deviation from the native asset value (NAV). Source

Despite the poor NAV tracking, however, Grayscale products can potentially be useful for investors.

There’s a Positive Correlation of Daily Price Change Between Grayscale Products and the Underlying Crypto Assets

We need to focus our analysis on the time periods where the price fluctuations of the Grayscale’s products were more stable. This means focusing our attention on the past 6 months.

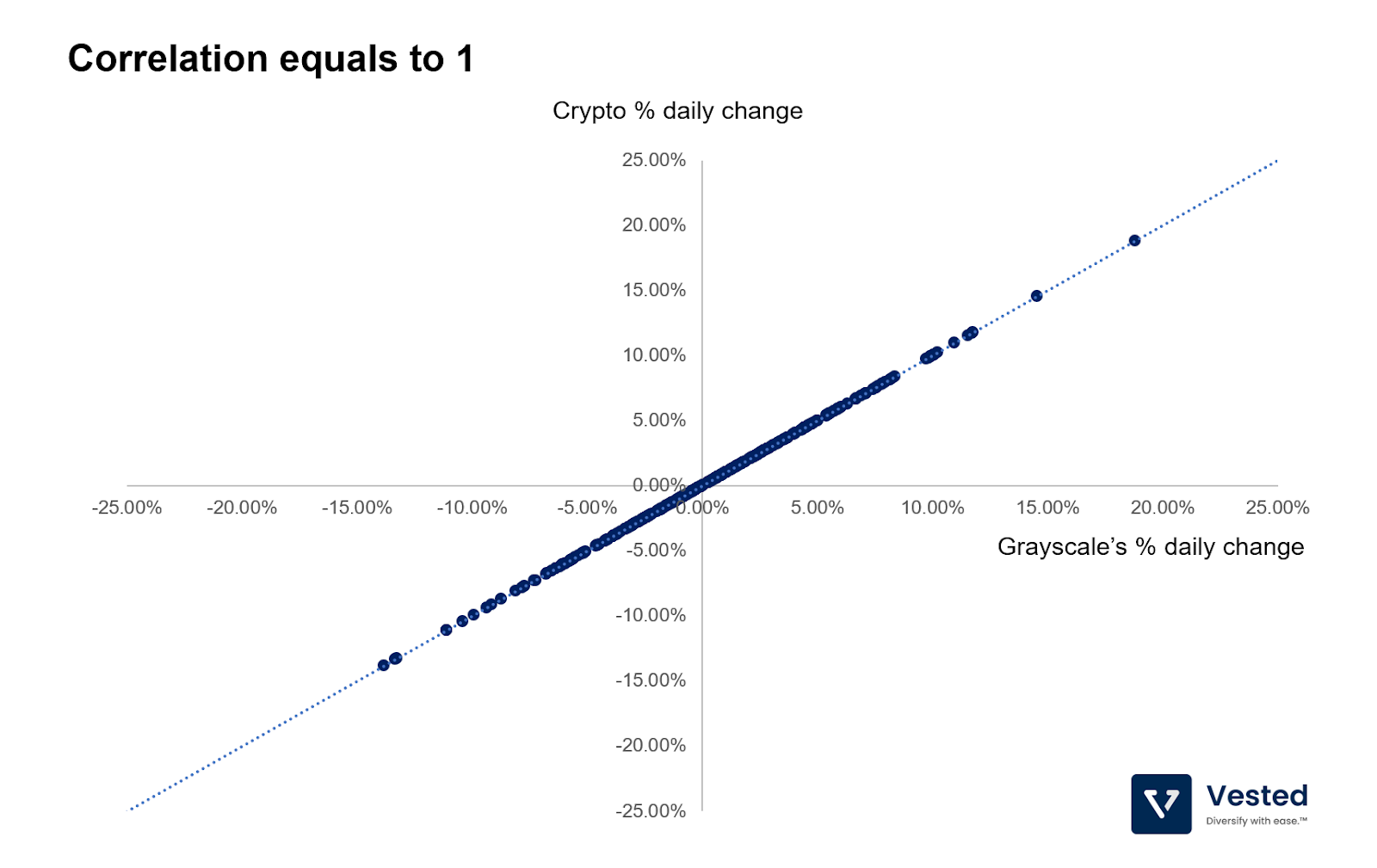

Let’s look at the relationship between the percentage daily change of the crypto vs. Grayscale’s product. If the crypto’s percentage daily change is perfectly tracked by the Grayscale products (in other words, correlation is one), then the relationship will look like a perfect line (Figure 4).

Figure 4: If correlation is one

But in reality, correlation is not one. There’s a spread between the movements of Grayscale’s share price and the underlying crypto. As you can see in Figure 5, The correlations are positive and tend to be lower than one (the blue dotted line has a less steep slope than the red dotted line, which represents perfect correlation).

Figure 5: Daily percent change of crypto vs. the Grayscale counterpart

How Does This Get Fixed?

Well, if Grayscale is successful in its application to convert its Trust into an ETF, then it will have the ability to address the supply and demand issue, eliminating the tracking error. If that happens, the discount will disappear. This is a BIG IF, however.

So far, the SEC has only approved BTC Futures (for example, BITO – we did a deep dive here) and not BTC spot ETF. Spot ETFs would be backed by the digital currency directly, rather than futures contracts. Many have tried to create the first BTC spot ETF and failed (Fidelity, Ark, VanEck, among others). This is due to a few unknowns:

- Where will the BTC come from? Unlike BITO, where the ETF is for futures contracts backed by the Chicago Mercantile Exchange (CME), which is an extension of current regulatory structure, where will the spot BTC ETF acquire its BTC? From which exchange? Many of the largest crypto exchanges in the world are not regulated by the SEC.

- Who will hold the BTC? Similarly, the SEC has not published a regulatory framework for custody of digital assets. The agency has asked for public comment, however.

These challenges are not deterring Grayscale from trying, however. Just last week, the FT reported that the company has submitted a new bid with the SEC. We shall know in July if their latest attempt is successful.

Disclaimer: “This guest post has been authored by the Vested team (https://vested.co.in/). All intellectual property in this post is property of Vested Finance Inc and its affiliates. This guest post has been published on our blog for your information and convenience only, and the contents thereof are not endorsed by ZebPay. ZebPay does not have control on the content of this guest post, and is not responsible for Vested’s website(s) or its content and availability.”